We use money to pay for things every day, yet most people never stop to ask what actually gives it value. A paper bill has no practical use on its own. A balance on a bank account is just a number in a database. Neither of those things has any inherent worth. What makes them work is something less tangible: collective trust, backed by law.

That is the foundation of fiat currency. And it is also exactly what cryptocurrency was designed to replace. Understanding what fiat money is, how it works, and where it falls short is the clearest way to understand what crypto is trying to solve.

What is fiat currency?

Fiat currency is money that a government declares to be legal tender. Its value does not come from any physical commodity like gold or silver. It comes from the authority of the state that issues it and the trust of the people who use it. The US dollar, the euro, the British pound, and the Japanese yen are all fiat currencies.

The word “fiat” comes from Latin and means “let it be done” or “by decree.” It refers to the fact that this money has value because a government says it does, not because it is backed by anything you can hold in your hand. As long as people trust that the currency will be accepted for payments and that the issuing government will remain stable, it functions as money.

Fiat currencies are managed by central banks: the Federal Reserve in the United States, the European Central Bank for the eurozone, the Bank of England in the UK. These institutions control how much money circulates in the economy, set interest rates, and respond to economic crises. Their decisions directly affect the purchasing power of the currency you hold.

A brief history of fiat money

Fiat currency did not appear overnight. It evolved over centuries from a series of earlier monetary systems, each with its own strengths and failures.

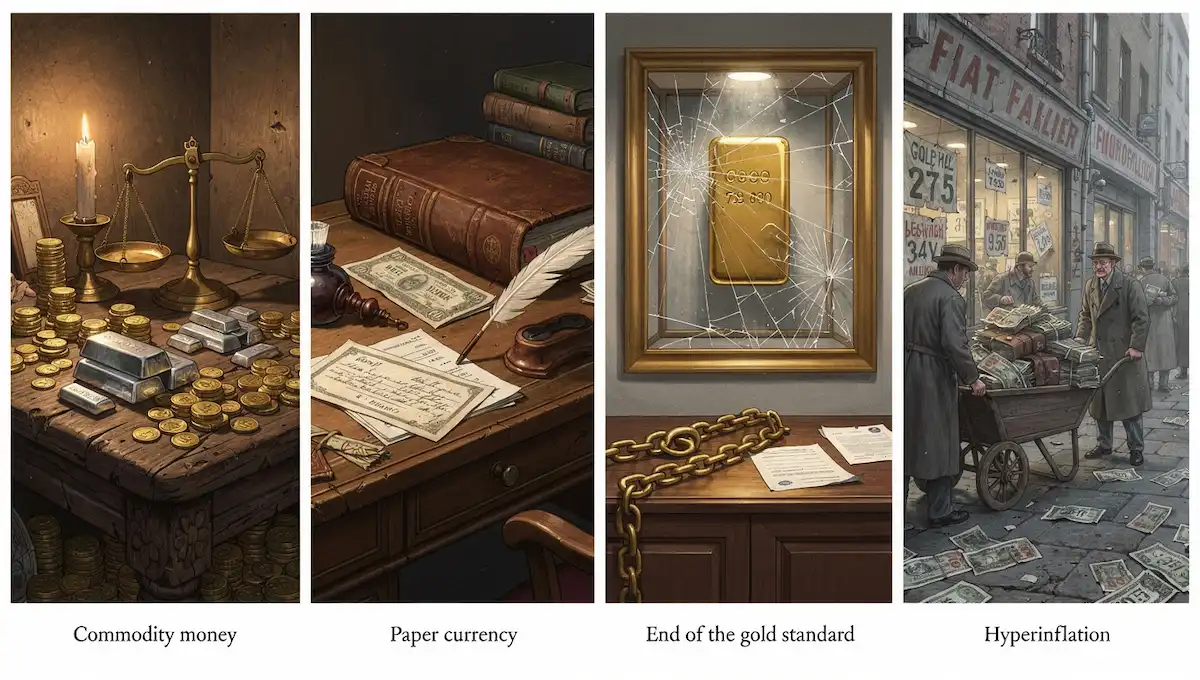

From commodity money to paper currency

Early money was commodity money: objects with inherent value like cattle, salt, or precious metals. Coins made from gold and silver were used for thousands of years because the metal itself was worth something. Paper money first appeared in China during the 11th century, but those early notes were still backed by metal held in reserve. This was representative currency: the paper represented a claim on a real commodity.

The shift to true fiat currency happened gradually, as governments found it useful to issue more paper money than they actually held in reserves. The trust placed in paper bills moved from “this note can be exchanged for gold” to “this note is accepted because the government says it is.”

The end of the gold standard

The clearest turning point came in 1971. After World War II, the Bretton Woods system had pegged global currencies to the US dollar, and the dollar was in turn backed by gold at a fixed rate of $35 per ounce. It was a managed form of the gold standard. In August 1971, President Nixon suspended the convertibility of the dollar into gold, effectively ending the gold standard for the entire global economy. Every major currency in the world became a fiat currency from that moment forward.

The change gave governments more flexibility to manage their economies, but it also removed the last external constraint on how much money they could create.

Hyperinflation: when fiat goes wrong

The risk built into fiat currency is that governments can print too much of it. When that happens, the currency loses value faster than people can adjust. The historical examples are stark.

In Germany in 1923, the Weimar Republic’s hyperinflation reached the point where a single US dollar was worth 4.2 trillion German papiermarks. People were paid twice a day so they could spend their wages before the value dropped further. In Zimbabwe in 2008, the government issued a 100 trillion dollar banknote that could not buy a loaf of bread. In Venezuela in 2019, inflation exceeded one million percent in a single year. These are extreme cases, but they demonstrate what happens when trust in a fiat currency collapses completely.

For more on how Bitcoin was created specifically as a response to the 2008 financial crisis and the failures of the fiat system, see our piece on who created Bitcoin.

How fiat currency works

Most people interact with fiat money daily without understanding the mechanics behind it. The system is more complex than it appears.

Who controls fiat money?

Central banks are the primary managers of a currency’s money supply. They do not print physical banknotes themselves in most cases; that role typically belongs to a government treasury or mint. But central banks control the broader money supply through three main tools:

- Interest rates: Raising rates makes borrowing more expensive, which reduces spending and slows the creation of new money through credit. Cutting rates does the opposite.

- Open market operations: Central banks buy or sell government bonds to add or remove money from the financial system. Buying bonds injects money; selling bonds withdraws it.

- Reserve requirements: Banks are required to hold a percentage of deposits in reserve rather than lending them out. Adjusting this requirement changes how much money banks can create through lending.

In theory, these mechanisms are run independently of political pressures. In practice, the line between central bank independence and government influence has been tested repeatedly throughout history, particularly when governments face large budget deficits.

What gives fiat money its value?

Three things hold a fiat currency together:

First, trust. When you accept a $50 bill, you do so because you believe the next person will also accept it. The entire system runs on shared confidence. If that confidence breaks, the currency fails, regardless of what any law says.

Second, legal tender laws. In most countries, fiat currency must legally be accepted as payment for debts. This creates a baseline demand for the currency that supports its value.

Third, tax obligations. Governments require taxes to be paid in the national fiat currency. This creates a continuous, non-optional demand for that currency from every individual and business operating within the country’s borders.

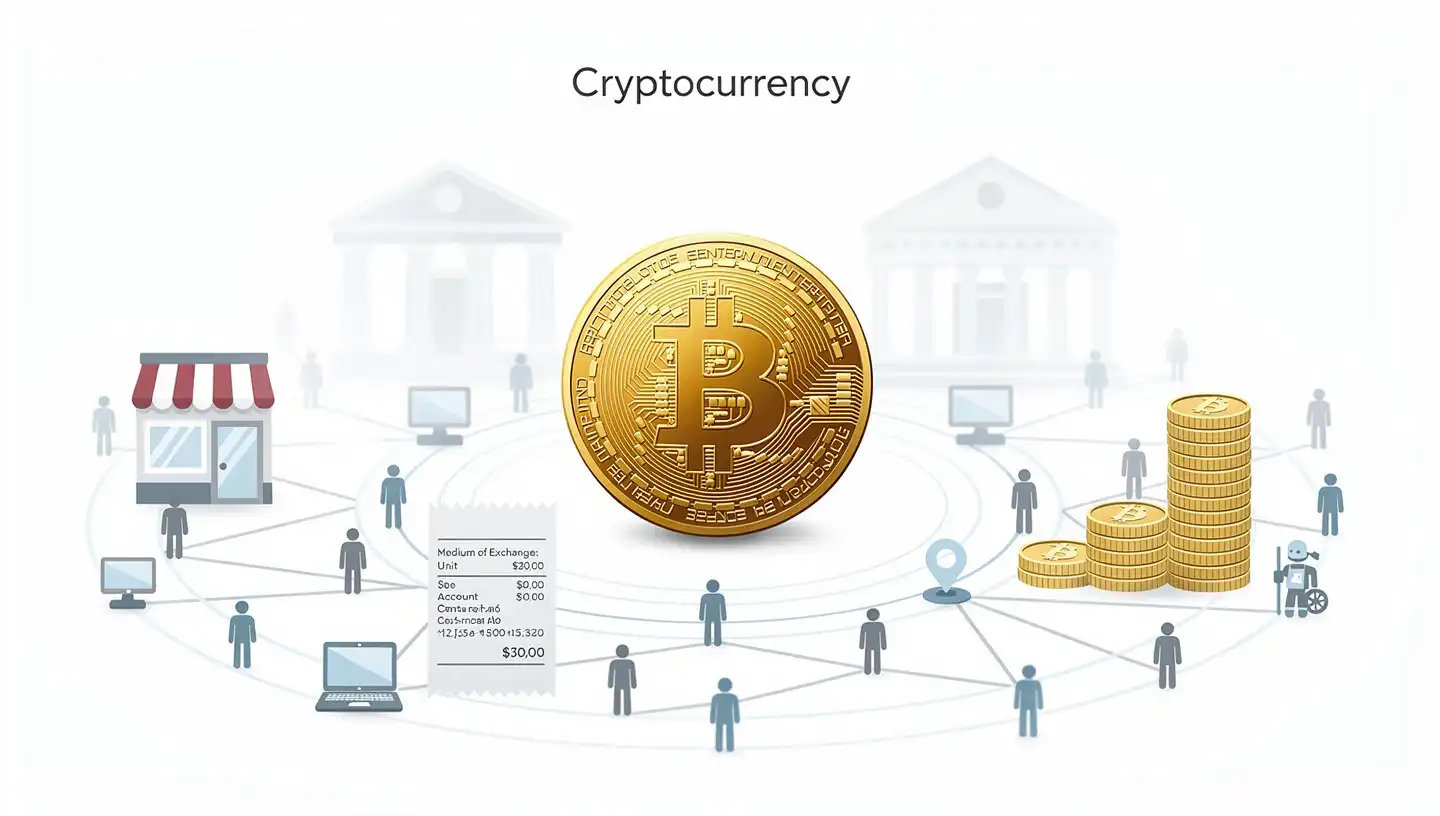

What is cryptocurrency?

Cryptocurrency is a form of digital money that operates on a decentralized network, with no central bank, no government issuer, and no single authority capable of changing the rules. Its value comes not from legal decree but from its underlying protocol, the security of its network, the limits built into its supply, and the demand of those who use and hold it.

Bitcoin was the first cryptocurrency, launched in January 2009 by an anonymous creator known as Satoshi Nakamoto. Its white paper described a peer-to-peer cash system that would allow two parties to transact directly without needing a financial institution in between. Every transaction is recorded on a blockchain, a public ledger maintained by a distributed network of participants around the world.

For money to function, economists generally say it must serve three purposes: act as a medium of exchange (accepted for payments), a store of value (hold worth over time), and a unit of account (used to price goods and services). Fiat currencies have served all three roles reliably within their respective economies. Cryptocurrencies are building toward the same but face different challenges at each stage.

For a full introduction to how cryptocurrency works as a category, see our guide on what is cryptocurrency.

Key differences between fiat currency and cryptocurrency

The differences between fiat and crypto go beyond one being physical and the other digital. They represent fundamentally different approaches to what money is and who should control it.

Control and governance

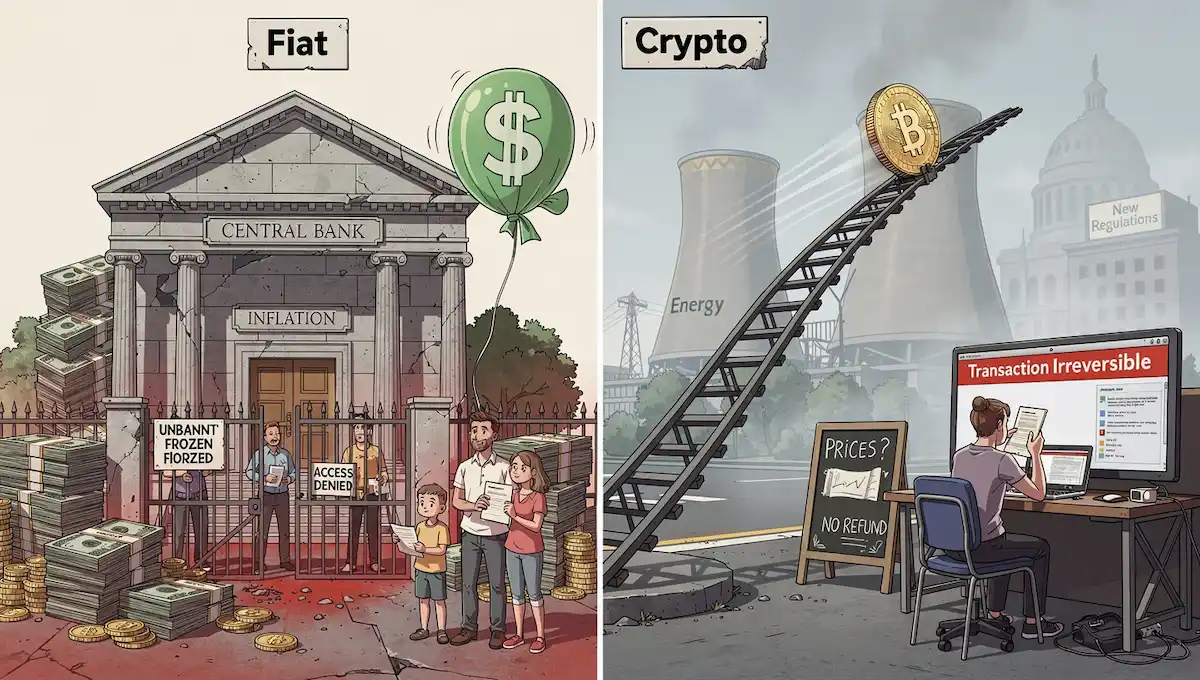

Fiat currency is centralized. The Federal Reserve can expand the money supply by buying bonds. The European Central Bank can set negative interest rates. A government can freeze a bank account. All of these actions are possible because there is a central authority with the power to make them.

Cryptocurrency is decentralized. No single entity controls the Bitcoin protocol. Changes to the rules require consensus from a majority of the network. No government can unilaterally create new bitcoins. No central bank can freeze a crypto wallet if the owner controls their own private keys. The system is described as “trustless” not because it is untrustworthy, but because trust in a person or institution is not required. The math and the code are the guarantors.

Supply and inflation

Fiat currencies have theoretically unlimited supply. A central bank can create new money whenever it decides the economy needs it. Whether through quantitative easing or direct money printing, the result is the same: more units in circulation, which tends to reduce the purchasing power of each existing unit. This is inflation, and it is a built-in feature of fiat systems, not a bug. The goal is a moderate, predictable rate that encourages spending and investment.

Bitcoin has a hard cap of 21 million coins. No more can ever be created. The rate at which new Bitcoin enters circulation halves approximately every four years in an event called the halving. This makes Bitcoin structurally deflationary over time, which is why some holders treat it as a hedge against the long-term erosion of fiat purchasing power.

For the full history of Bitcoin’s supply mechanics and price development, see our Bitcoin history guide.

Transaction speed and fees

Domestic fiat transactions, such as paying with a card at a shop or making a bank transfer within the same country, are fast and cheap. International fiat transfers are a different story. Moving money across borders through the traditional banking system can take one to five business days and carries fees that often range from 3-7% of the amount transferred. Wire services like Western Union charge flat fees plus exchange rate markups. For low-income migrant workers sending money home, these costs represent a significant percentage of what they earn.

Cryptocurrency international transfers can settle in minutes rather than days. Fees vary significantly by network. Bitcoin fees fluctuate with congestion and can be several dollars per transaction. XRP and Solana process transfers in seconds at fractions of a cent. The advantage is most pronounced for large international transfers, where a $20 billion interbank settlement costs the same in fees as a $200 transfer on most crypto networks.

Privacy and transparency

Fiat currency digital transactions are tracked extensively. Every card payment, bank transfer, and online purchase creates a record tied to your identity. Banks are legally required to report suspicious transactions to authorities. Governments can obtain transaction histories, freeze accounts, and block payments. Cash provides more privacy but is increasingly restricted in high-value transactions across many countries.

Cryptocurrency transactions are recorded on a public blockchain. Anyone can see the full transaction history of any wallet address. What they cannot immediately see is who owns that address. The system is pseudonymous rather than anonymous: transactions are visible, identities are not directly attached. Sophisticated blockchain analysis can sometimes link addresses to real identities, especially when crypto is converted back to fiat through regulated exchanges that require identity verification.

Accessibility and financial inclusion

An estimated 1.4 billion adults worldwide have no bank account, according to World Bank financial inclusion data. Opening a bank account requires identification documents, a physical address, minimum balance requirements, and proximity to banking infrastructure. For hundreds of millions of people in developing countries, these barriers are insurmountable.

Cryptocurrency requires only an internet connection and a smartphone to use. No ID is needed to create a wallet. No minimum balance. No branch to visit. This is why crypto has seen significant adoption in countries with weak banking systems, high inflation, or unstable governments. The practical limitation is that converting between crypto and local currency still often requires going through an exchange with its own verification requirements.

Security model

Fiat currency is protected by a centralized security model. If someone steals from your bank account through fraud, the bank can reverse the transaction and restore your funds. Deposits in most developed countries are insured up to a certain limit by government-backed schemes. The system assumes errors can be corrected because a central authority has that power.

Cryptocurrency’s security model is the opposite. Transactions are irreversible once confirmed. If someone gains access to your private key and drains your wallet, there is no support desk, no insurance, and no reversal. The cryptographic security of the blockchain itself is extremely strong. The vulnerability is at the human layer: stolen keys, phishing attacks, compromised exchanges. Self-custody means full control and full responsibility simultaneously.

| Feature | Fiat currency | Cryptocurrency |

|---|---|---|

| Control | Centralized (governments and central banks) | Decentralized (protocol and network) |

| Supply | Unlimited (can be increased by central banks) | Fixed or programmatic (e.g. 21M BTC cap) |

| Inflation | Prone to inflation through money creation | Deflationary potential for capped assets |

| Transaction speed | Fast domestically, slow internationally | Fast to very fast depending on network |

| International fees | High (3-7% typical for remittances) | Low to very low on most networks |

| Privacy | Low (tracked and monitored) | Pseudonymous (public ledger, hidden identity) |

| Accessibility | Requires banking infrastructure and ID | Requires internet and smartphone only |

| Error correction | Transactions can be reversed | Transactions are irreversible |

| Legal status | Legal tender in issuing country | Varies by country, generally not legal tender |

| Volatility | Low (in stable economies) | High for most assets |

For a technical breakdown of how proof-of-work and proof-of-stake networks verify transactions differently, and what that means for crypto’s role as a currency, see our guide on proof of work vs proof of stake.

Advantages of fiat currency

- Universal acceptance. Every shop, every service, every government office accepts fiat. There is no need to check whether a merchant supports it or to explain what it is.

- Price stability. In well-managed economies, fiat currencies hold their value predictably enough for people to plan financially over years and decades. Mortgages, pensions, and long-term contracts all depend on this relative stability.

- Regulatory protection. Fiat transactions come with legal frameworks. If a bank commits fraud, there are laws and regulators with enforcement power. Deposits are insured. Consumer protection laws apply.

- Integration with financial services. Loans, mortgages, insurance, investment accounts, and tax systems: the entire financial infrastructure of the modern economy is built on fiat. These products are mature, accessible, and widely understood.

- Crisis management. When economies go into recession, central banks can cut rates and create money to stimulate activity. This flexibility has genuine value: it helped prevent a global depression in 2008 and funded emergency responses to COVID-19 in 2020.

Advantages of cryptocurrency

- No central authority. No government can confiscate crypto held in a self-custodied wallet, freeze it, or devalue it by printing more. For people in countries with unstable governments or histories of financial repression, this matters significantly.

- Lower cost for international transfers. Moving money across borders in crypto costs a fraction of what wire transfers and remittance services charge. The difference is meaningful for migrant workers who regularly send money home.

- Financial access without banks. Anyone with a phone and internet access can hold and transfer value in crypto without needing to qualify for a bank account.

- Programmable transactions. Smart contracts enable financial agreements that execute automatically when conditions are met, with no intermediary required. This capability has no equivalent in the fiat system.

- Transparent supply. Every bitcoin that exists and every one that will ever be created is accounted for in the public protocol. There is no equivalent transparency in the fiat money system.

For more on how smart contracts work and what they enable beyond simple payments, see our guide on what is a smart contract.

Challenges and limitations of both

Fiat currency challenges

The core vulnerability of fiat currency is that its value depends entirely on the competence and integrity of the institutions that manage it. Inflation erodes purchasing power even in well-run systems; the US dollar has lost roughly 97% of its purchasing power since the Federal Reserve was established in 1913. Currency devaluation can be used as a policy tool in ways that redistribute wealth from savers to borrowers without transparency. Governments can also freeze accounts, block transactions, and exclude specific individuals or organizations from the financial system, all of which are forms of centralized power that some people find problematic.

For the unbanked population, fiat currency’s dependence on traditional banking infrastructure means the system simply does not serve them at all.

Cryptocurrency challenges

Crypto’s most persistent problem is volatility. Bitcoin has lost more than 80% of its value in a single bear market on multiple occasions. A currency that can drop by half in a month is not suitable for paying rent or setting prices. This limits crypto’s usefulness as a medium of exchange for everyday transactions, even as its properties as a long-term store of value attract interest from institutional investors.

The regulatory environment remains uncertain in most countries. What is legal and accessible today may face new restrictions tomorrow. Energy consumption for proof-of-work networks remains a genuine concern: Bitcoin’s mining network consumes more electricity annually than many smaller countries. And the irreversibility of transactions means there is no recourse for mistakes or fraud, which represents a real barrier for mainstream adoption.

Stablecoins and CBDCs: bridging fiat and crypto

The strict division between fiat and crypto has been blurring. Two categories of assets sit at the intersection of both systems.

Stablecoins are cryptocurrencies pegged to a fiat currency, almost always the US dollar. Tether (USDT) and USD Coin (USDC) are the two largest. Each token is meant to be worth exactly $1, backed by cash and short-term bonds held in reserve by the issuing company. They combine the speed, accessibility, and programmability of crypto with the price stability of fiat. Most decentralized finance activity is denominated in stablecoins rather than volatile cryptocurrencies.

Central Bank Digital Currencies (CBDCs) take the reverse approach. They are digital fiat currencies issued directly by central banks on distributed ledger technology. China’s digital yuan (e-CNY) is the furthest along in real-world deployment, with tens of millions of users already. The European Central Bank is developing a digital euro. The United States is actively researching a digital dollar. The Atlantic Council’s CBDC tracker shows that more than 130 countries are now at some stage of CBDC development. A CBDC would be fully controlled by the central bank, programmable, traceable, and revocable, and it would represent the direct opposite of what Bitcoin was designed to be, even though both exist as digital entries on a ledger.

The critical distinction: a stablecoin is a private company’s promise to maintain a peg using reserves it controls. A CBDC is a direct liability of the central bank. The trust model is entirely different.

For more on how DeFi protocols use stablecoins and what that means for the relationship between fiat and crypto, see our guide on what is DeFi.

Fiat vs. crypto: which is better?

They serve different needs and are not direct substitutes for each other. Declaring one “better” misses the point.

Fiat is better for everyday purchases, price stability, legal protection, and integration with the financial services most people depend on. As long as the issuing government is stable, fiat currency works reliably for the vast majority of financial activity in developed economies.

Crypto is better for international transfers without intermediaries, financial access in regions with limited banking infrastructure, protection against currency devaluation in unstable economies, and programmable financial applications that have no fiat equivalent. Bitcoin’s track record as a long-term store of value has attracted serious institutional investment, though its short-term volatility remains a genuine limitation.

The most realistic outcome is not one replacing the other. It is coexistence and gradual convergence. CBDCs will bring central bank money closer to the properties of crypto. Stablecoins already operate in both worlds. Payment processors are integrating crypto options alongside traditional fiat. The boundary between the two systems is more porous in 2026 than it was in 2019, and that trend is likely to continue.

For a practical guide to getting started with cryptocurrency, including how to buy, store, and evaluate different assets, see our crypto for beginners guide.

Frequently asked questions

What does “fiat” mean in fiat currency?

The word comes from Latin and means “let it be done” or “by decree.” In monetary terms, it describes currency that has value because a government declares it legal tender, not because it is backed by a physical commodity. The US dollar has been a fiat currency since 1971 when the United States ended the convertibility of the dollar into gold.

Is cryptocurrency legal tender?

In most countries, no. El Salvador adopted Bitcoin as legal tender in 2021, making it the first country to do so. The Central African Republic followed briefly before reversing course. Most governments have not granted legal tender status to any cryptocurrency, meaning businesses are generally not legally required to accept it as payment. That said, many do by choice.

Can crypto replace fiat money?

Not in the near term, and possibly not at all in the way the question implies. Replacing fiat would require crypto to achieve price stability, universal acceptance, regulatory integration, and the kind of widespread trust that fiat currencies have built over generations. Stablecoins and CBDCs are more likely to gradually merge the properties of both systems than for any single cryptocurrency to replace national currencies outright.

Why does fiat currency have value if it is not backed by gold?

Because governments require taxes to be paid in it, laws require it to be accepted for settling debts, and billions of people agree to use it daily. Value in a currency system comes from trust and utility, not from a physical commodity. Gold-backed money was itself only valuable because people agreed gold was valuable, which is the same trust-based logic, just with an extra step in the middle.

What is the main advantage of crypto over fiat?

Depends on the use case. For international transfers, the main advantage is lower cost and faster settlement without intermediaries. For people in countries with high inflation or unstable governments, the main advantage is a store of value not subject to local monetary policy. For developers, the main advantage is programmability through smart contracts.

Which is safer: fiat or crypto?

They carry different risks. Fiat is protected by legal systems and deposit insurance but is vulnerable to inflation, government control, and the financial stability of the issuing state. Crypto is protected by cryptography and is not subject to inflation or seizure if you control your own keys, but is vulnerable to user error, exchange failures, scams, and high price volatility. Neither is categorically safer; the right answer depends on what specific risk you are trying to protect against.

What are stablecoins and how do they relate to fiat?

Stablecoins are cryptocurrencies pegged to the value of a fiat currency, almost always the US dollar. Tether (USDT) and USD Coin (USDC) are the largest. Each token is designed to be worth $1, backed by cash reserves held by the issuing company. They combine the price stability of fiat with the technical properties of crypto: transferable on blockchain networks, usable in DeFi applications, and accessible globally without a bank account.

Do I pay taxes on crypto the same way as fiat?

In most countries, no. Fiat currency income is taxed as ordinary income. Cryptocurrency is typically treated as property, not currency, for tax purposes. Selling crypto for a profit, trading one crypto for another, or using crypto to buy goods and services can all trigger taxable events. The specific rules vary by country and are still evolving. Keeping records of all transactions from the start is essential, and consulting a tax professional familiar with crypto in your jurisdiction is the safest approach.