A blockchain is a shared digital ledger that records transactions across a network of computers. No single person or organisation controls it. Once a record is added, it cannot be changed without altering every block that follows it, which makes the data effectively permanent. Bitcoin was the first application of this technology, launched in 2009, but blockchain is now used far beyond cryptocurrency, in supply chains, healthcare, finance, and legal contracts.

This guide explains what a blockchain is, how it works from the moment a transaction starts to the moment it is permanently recorded, and what separates it from a regular database.

- A blockchain is a shared digital ledger copied across thousands of computers simultaneously

- Transactions are grouped into blocks and linked together using cryptographic codes called hashes

- Once added, a block cannot be changed without breaking the entire chain

- Bitcoin was the first blockchain application, but the technology now powers far more than cryptocurrency

- No central authority, bank, or government controls a public blockchain

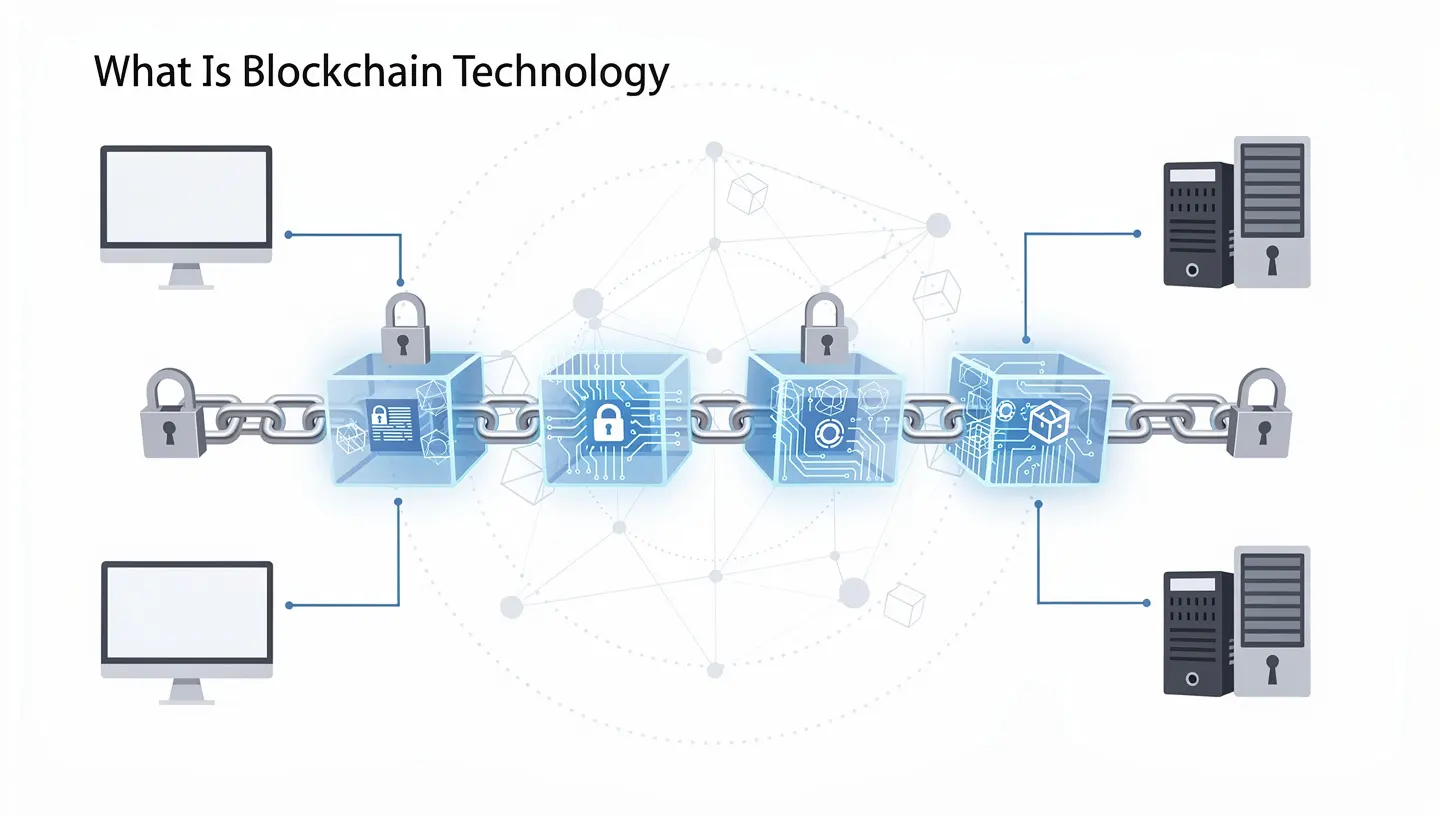

What is blockchain?

A blockchain is a type of distributed ledger, a database that is copied and shared across many computers at the same time rather than stored in one central location. Every participant on the network holds an identical copy of the same record. When a new transaction is added, every copy updates at the same time.

The name comes from the structure itself. Transactions are grouped into blocks. Each block is connected to the one before it, forming a chain. The chain is ordered chronologically, so the complete history of every transaction is visible to anyone who checks it.

What makes this different from a normal database is the combination of two things: no single party controls it, and once something is written, it cannot be erased or quietly changed. That combination is what makes blockchain useful in situations where two parties do not fully trust each other but both need to rely on the same record.

Why was blockchain invented?

Before blockchain existed, any digital payment system needed a trusted middleman, a bank or payment processor, to confirm that money had not been spent twice. If you sent someone a digital file, you could still keep a copy. Digital money had the same problem: without a central authority checking balances, you could theoretically spend the same coin in two places at once. This was known as the double-spending problem.

In October 2008, a person or group using the name Satoshi Nakamoto published a paper called “Bitcoin: A Peer-to-Peer Electronic Cash System.” It described a method for recording transactions on a public ledger maintained by a network of computers, with no bank or government involved. The Bitcoin network went live on 3 January 2009. The blockchain was the technology underneath it.

Satoshi Nakamoto’s real identity has never been confirmed. After handing the Bitcoin code to other developers in 2010, the name disappeared from public view entirely. What remained was a working system that solved the double-spending problem without relying on any third party.

You can read the full story in our guide to Bitcoin history: from $0 to all-time highs.

How does blockchain work?

The process that takes a transaction from initiation to permanent record involves four steps.

Each one is handled by the network automatically, without any central authority overseeing it.

Step 1: a transaction is initiated

A blockchain transaction represents the movement of any asset from one address to another. In a cryptocurrency network, that asset is a coin or token. In a supply chain network, it might be a record that a shipment has left a warehouse. The transaction includes details about who sent it, who received it, when it happened, and how much was transferred.

Before anything is broadcast to the network, the transaction is signed with the sender’s private key. In crypto, a private key is a cryptographic code that proves the sender owns the asset they are trying to transfer. Anyone can verify the signature using the corresponding public key, but only the holder of the private key can create the signature in the first place. This is how ownership is established without a bank checking your account.

Step 2: the transaction is broadcast to the network

Once signed, the transaction is sent to the network. The computers participating in the network are called nodes. Each node receives the transaction and checks it against its own copy of the ledger. If the sender has the funds or assets they claim to have, the transaction is considered valid. If not, it is rejected.

This is a peer-to-peer process. There is no central server that handles the checking. Every node does its own verification independently, and the results are compared across the network.

Step 3: nodes reach agreement through a consensus mechanism

For a transaction to be added to the blockchain, the majority of nodes must agree it is valid. This agreement process is called a consensus mechanism. The two most widely used are proof of work and proof of stake.

In proof of work, computers compete to solve a complex mathematical puzzle. The first computer to solve it earns the right to add the next block and receives a reward in cryptocurrency. Bitcoin uses proof of work. It is secure but requires significant computing power and energy.

In proof of stake, validators are chosen based on how much cryptocurrency they have locked up as collateral. Ethereum switched to proof of stake in September 2022. It uses far less energy than proof of work and achieves the same result: agreement across the network without any central authority making the decision.

Step 4: the block is added to the chain

Once the network reaches consensus, the verified transactions are collected into a block. Each block contains three things: the transaction data, a timestamp, and a cryptographic hash.

A hash is a fixed-length string of characters generated from the data inside the block. Change even one character of the data and the hash changes completely. Each block also contains the hash of the block before it. This is what creates the chain: each block references the previous one, going all the way back to the first block ever created, which is called the genesis block.

Once the block is added, the updated ledger is distributed to every node on the network simultaneously. Every copy reflects the new state.

What makes blockchain records impossible to change?

This is the property that most people mean when they call blockchain “trustless.” The word does not mean the system is untrustworthy. It means you do not need to trust any individual person or organisation to keep the record accurate. The record keeps itself accurate through the structure of the chain.

Here is why changing a record is not practical. Suppose someone wanted to alter a transaction recorded three blocks ago. They would have to:

- Change the data in that block, which changes its hash

- Recalculate the hash of every subsequent block, because each one contains the hash of the block before it

- Redo all of this faster than the rest of the network is adding new blocks

- Control more than half the computing power on the entire network simultaneously

On a large network like Bitcoin, that last requirement means controlling thousands of computers running around the clock. The cost of attempting this, known as a 51% attack, would far exceed any possible gain. On smaller networks the risk is real, which is one of the reasons not all blockchains are equally secure.

This combination of cryptographic hashing and distributed consensus is what makes blockchain records immutable: effectively permanent once confirmed.

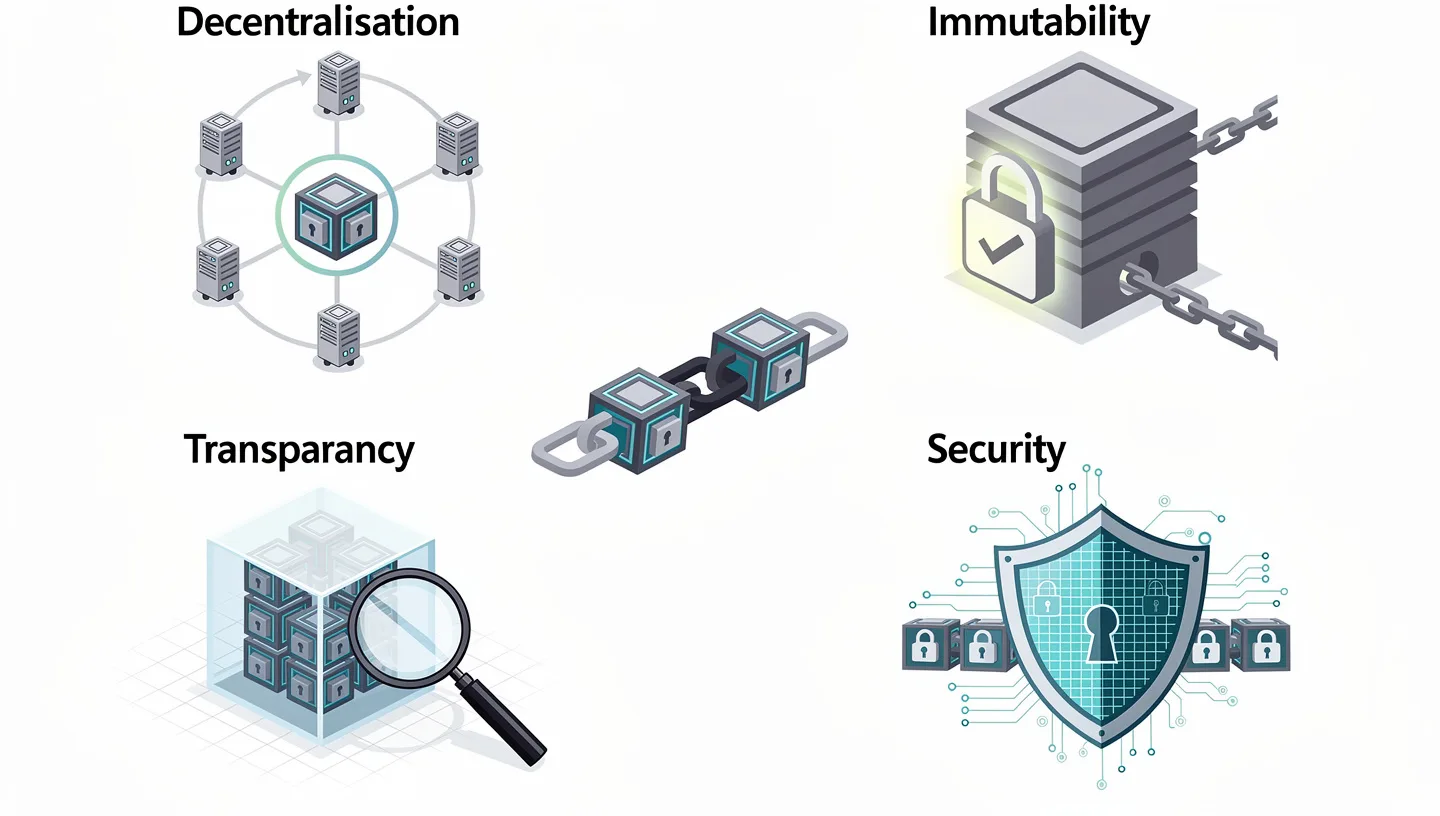

What are the main properties of blockchain?

Four properties define how blockchain behaves and why it is trusted in the applications where it is used.

Decentralisation

Decentralisation means no single entity controls the network. In a traditional financial system, a bank maintains the ledger, and you have to trust the bank to record transactions accurately and keep the database secure. In a public blockchain, thousands of independent computers maintain identical copies of the same ledger. No one can shut down the network by disabling a single server, and no single participant can alter the record unilaterally.

Immutability

Immutability means records cannot be changed after the fact. The cryptographic link between blocks and the requirement for network consensus make retroactive changes computationally impractical. This is what makes blockchain suitable for audit trails, title records, and financial transactions where a permanent, unaltered history matters.

Transparency

On a public blockchain, every transaction is visible to anyone who looks. The identities behind the wallet addresses are not necessarily known, but the transactions themselves are fully visible. This transparency allows anyone to verify the record independently without asking permission. It also makes fraud harder to conceal, because the entire history is open to inspection.

Security

Blockchain uses cryptography at two levels. First, each participant’s identity and ownership is established through public and private key pairs. Second, the data inside each block is secured by its hash. The combination makes the data resistant to tampering and forgery. That said, the security of a blockchain is only as strong as its network size and the quality of its consensus mechanism. A small network with few nodes is meaningfully more vulnerable than a large one.

How is blockchain different from a regular database?

Blockchain is a type of database, but it works very differently from the databases that power most websites and applications. The comparison matters because a lot of the hype around blockchain involves replacing databases with blockchains in contexts where a regular database would work better.

| Feature | Regular database | Blockchain |

|---|---|---|

| Control | Central administrator | Distributed network of nodes |

| Can data be edited? | Yes, by authorised users | No, only new records can be added |

| Can data be deleted? | Yes | No |

| Trust model | Trust the administrator | Trust the network consensus |

| Speed | Very fast | Slower, limited by consensus process |

| Best suited for | Internal records, fast updates | Shared records, multiple parties |

A regular database is the right tool when one organisation controls the data and speed matters. A blockchain is the right tool when multiple parties who do not fully trust each other need to share a record and no one party should be in charge of it. Using blockchain where a regular database would do the job adds cost and complexity without any benefit.

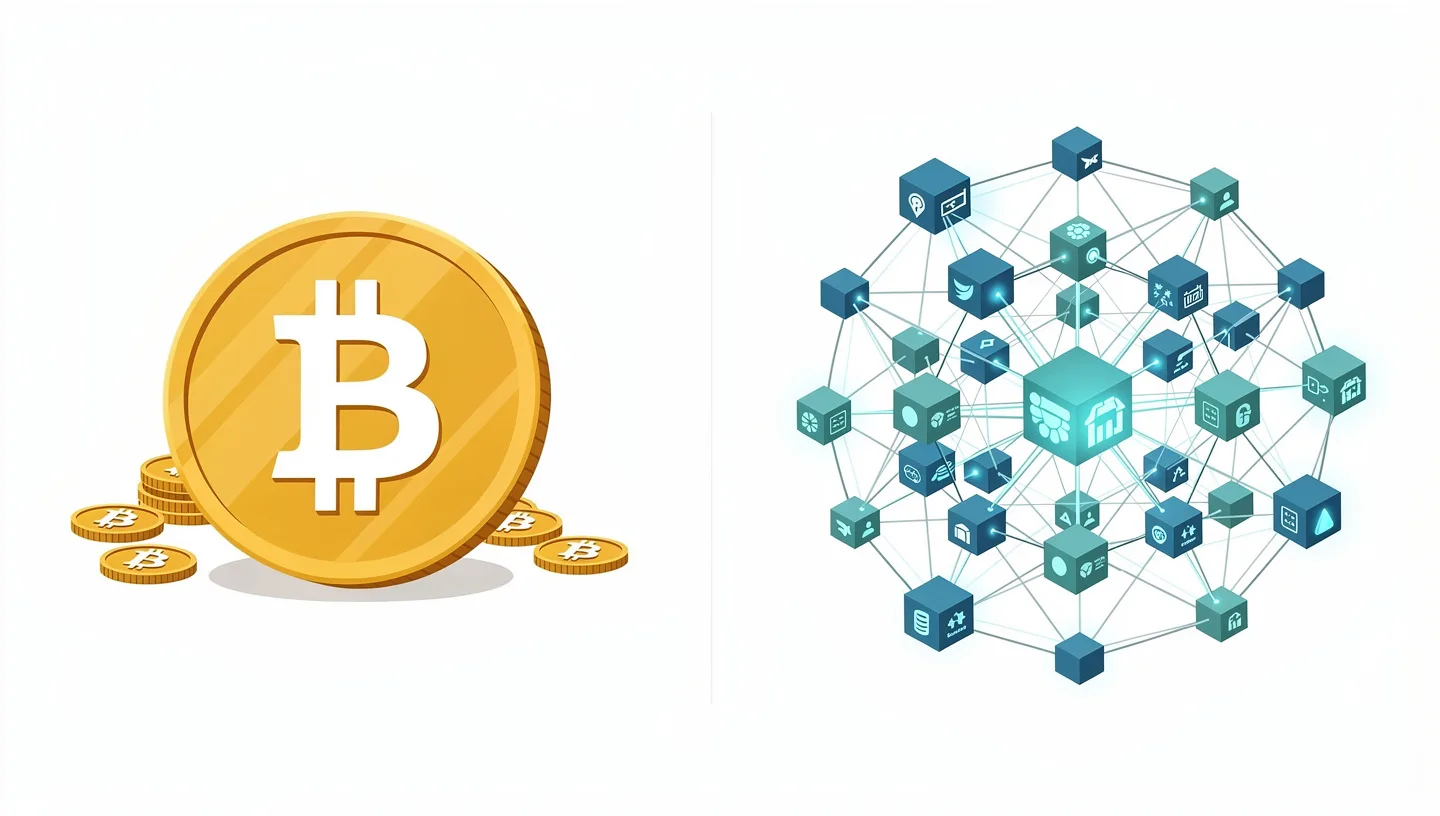

What is the difference between blockchain and Bitcoin?

Bitcoin is a cryptocurrency. Blockchain is the technology it runs on. The two are often used as if they mean the same thing, partly because Bitcoin was the first major application of blockchain and brought the technology to public attention.

Bitcoin uses one specific blockchain: the Bitcoin blockchain, a public ledger that records every Bitcoin transaction ever made. But blockchain technology exists independently of Bitcoin. Ethereum has its own blockchain. Thousands of altcoins, which are any cryptocurrencies other than Bitcoin, run on their own blockchains or on shared ones. Most altcoins are either native coins of their own network or tokens built on top of an existing blockchain like Ethereum. The distinction between a coin and a token matters for understanding how these assets work at a technical level. Private companies run blockchains with no cryptocurrency involved at all.

The relationship is similar to the internet and email. Email runs on the internet, but the internet is not email. Bitcoin runs on a blockchain, but blockchain is not Bitcoin.

For a full explanation of what Bitcoin is, how it works, and how it processes transactions, see our guide to what is Bitcoin.

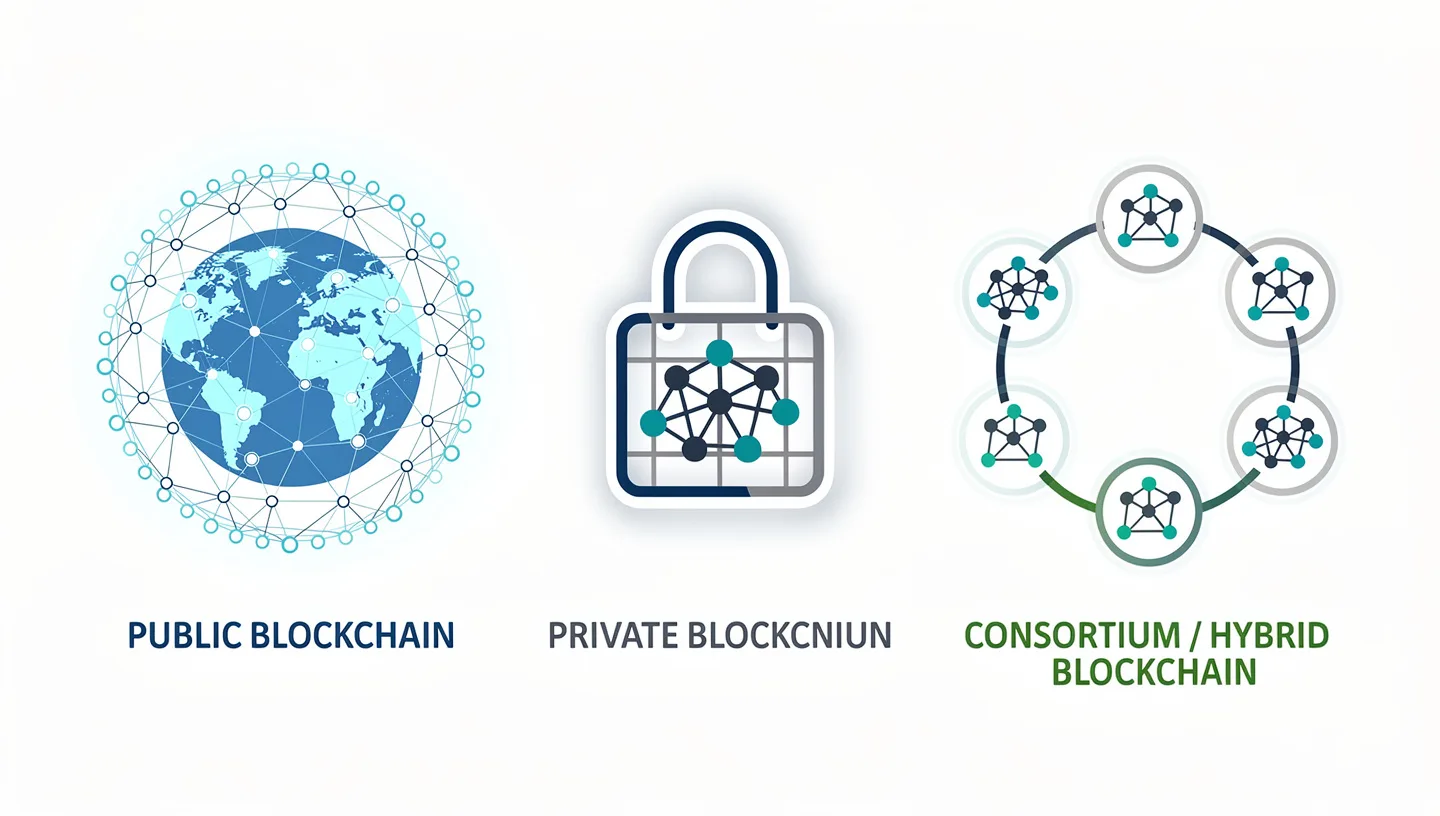

What are the types of blockchain?

Not all blockchains are open to the public.

There are three main types, each suited to different situations.

Public blockchains

A public blockchain is open to anyone. Anyone can read the ledger, send transactions, or run a node. Bitcoin and Ethereum are public blockchains. They are the most decentralised type because no single organisation controls who participates. Every transaction is visible to anyone, which is why public blockchains are the foundation for cryptocurrency as it is commonly understood. The tradeoff is that they are slower and more expensive to run than private alternatives, because consensus across thousands of independent nodes takes time.

Private blockchains

A private blockchain is controlled by a single organisation that decides who can participate, read the ledger, and add new blocks. It is faster and cheaper than a public blockchain but gives up the core property of decentralisation. A private blockchain is really a shared database with extra features. It makes sense in business contexts where the participants are known, trusted, and operating under the same legal framework.

Consortium and hybrid blockchains

A consortium blockchain is governed by a group of organisations rather than a single one. Each member has partial control over the network. It is common in industries where multiple competing companies need to share data, such as banking, shipping, or pharmaceuticals. A hybrid blockchain combines elements of public and private models, letting organisations choose which data is visible to the public and which is restricted.

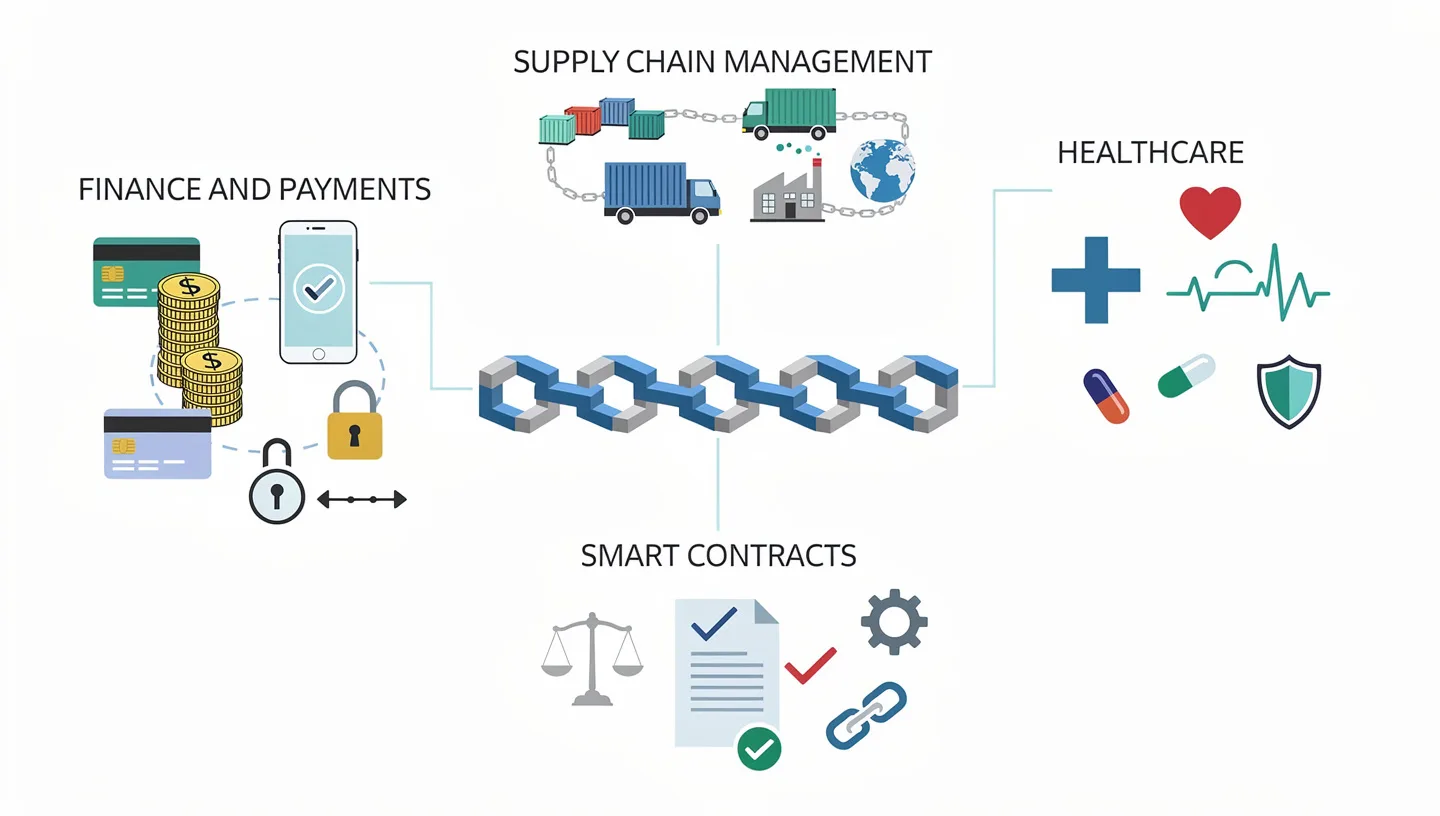

What is blockchain used for?

Blockchain started as the infrastructure for Bitcoin, but its properties, a shared, tamper-resistant, transparent record, turn out to be useful in many other contexts.

Here are the most significant ones.

Finance and payments

Beyond cryptocurrency, banks and financial institutions use blockchain to settle transactions between institutions, reduce the need for reconciliation between separate databases, and speed up cross-border payments. A transfer that takes three business days through a traditional correspondent banking network can settle in minutes on a blockchain.

Singapore Exchange Limited, for example, used blockchain to rebuild its interbank payment infrastructure and eliminate manual reconciliation across thousands of daily transactions. The total market cap of assets settled on blockchain networks now runs into the trillions of dollars, a figure that covers Bitcoin, Ethereum, stablecoins, and tokenised assets across multiple industries.

Supply chain management

Every time a product moves from a manufacturer to a distributor to a retailer, it generates a record. Those records currently live in separate systems that do not talk to each other. A shared blockchain ledger gives every participant in the supply chain the same view of the same data. If a product recall is needed, the source can be traced in hours rather than weeks. Amazon has patented a blockchain-based system to verify the authenticity of goods sold on its platform.

Healthcare

Medical records are stored across hospitals, GP practices, specialists, and pharmacies that use incompatible systems. A blockchain-based health record could give a patient’s complete history to any authorised provider without requiring data transfers between institutions. The patient controls who can see their records through their private key, and every access is logged permanently on the ledger.

Smart contracts

A smart contract is a program stored on a blockchain that runs automatically when predefined conditions are met. No third party is needed to enforce it. A simple example: a logistics company writes a smart contract that releases payment to a supplier the moment a shipment is confirmed delivered. The contract checks the condition and executes the payment without anyone having to approve it manually.

Smart contracts are the foundation of decentralised finance (DeFi), where lending, borrowing, and trading happen through code on a blockchain rather than through a bank or broker. You can read how DeFi works in our guide to what is DeFi.

What are the limits of blockchain?

Blockchain solves real problems but it creates new ones, and understanding them is part of understanding the technology honestly.

Speed. A public blockchain like Bitcoin processes roughly seven transactions per second. Visa processes tens of thousands per second. The consensus mechanism that makes blockchain secure is also what makes it slow. Every node must agree before a new block is added, and that takes time. Various solutions exist, including Layer 2 networks that process transactions off the main chain and settle them in batches, but the base layer remains slower than centralised alternatives.

Energy consumption. Proof-of-work blockchains like Bitcoin require significant computing power to run the puzzle-solving competition that adds new blocks. The Bitcoin network consumes more electricity annually than some mid-sized countries. Proof-of-stake networks like Ethereum use far less energy, but proof of work remains dominant for the largest cryptocurrency network.

Scalability. As a blockchain grows, the amount of data every node must store grows with it. The Bitcoin blockchain is now over 600 gigabytes. Storing and processing this much data puts pressure on nodes and limits who can practically participate in the network.

Irreversibility. The immutability that makes blockchain trustworthy also means mistakes cannot be undone. If you send cryptocurrency to the wrong address, there is no customer service number to call. If a smart contract has a bug, it executes the buggy code. The code is the contract, and the contract is permanent.

The 51% attack risk on small networks. On a large, well-established blockchain like Bitcoin, controlling 51% of the network’s computing power would require billions of dollars of hardware and energy. On a small, newer blockchain, the same attack might cost thousands. Several smaller blockchains have suffered 51% attacks resulting in double-spending. Network size directly affects security.

The bottom line

Blockchain is a method of recording information that removes the need for a central trusted authority. It does this by distributing an identical copy of the ledger across thousands of independent computers, linking records together with cryptographic codes that make them effectively impossible to change, and requiring the network to agree before anything is added.

The technology works. Bitcoin has run continuously since 2009 without a single instance of the ledger being compromised. Ethereum has processed billions of transactions. Supply chains, financial institutions, and healthcare networks are building on the same foundations.

What blockchain does not do is make every problem easier. It is slower and more expensive to operate than a regular database. It makes sense when multiple parties who do not trust each other need to share a permanent record. It does not make sense as a replacement for a regular database just because it is new.

For a wider view of how blockchain fits into the cryptocurrency space, the original Bitcoin whitepaper by Satoshi Nakamoto remains the clearest first-principles explanation of the technology, and the Ethereum Foundation’s introduction to Ethereum shows how blockchain was extended beyond currency into programmable contracts.

Frequently asked questions

Is blockchain the same as cryptocurrency?

No. Blockchain is the underlying technology and cryptocurrency is one application of it. Bitcoin runs on a blockchain, but blockchain is used in supply chains, healthcare, legal contracts, and many other fields that have nothing to do with digital currency. Think of blockchain as the infrastructure and cryptocurrency as one of many things built on top of it.

Can blockchain be hacked?

The data recorded on a large, established blockchain like Bitcoin has never been successfully altered. The cryptographic structure and the distributed consensus mechanism make tampering computationally impractical. However, smaller blockchains with fewer nodes are vulnerable to what is called a 51% attack, where an attacker controls enough of the network to rewrite recent transactions. The wallets and exchanges that hold cryptocurrency can also be hacked, even if the blockchain itself cannot.

Who controls a blockchain?

On a public blockchain, no single person or organisation is in control. The network of nodes that maintain the ledger collectively governs it. Changes to how the blockchain works require broad agreement from the network. Private blockchains are controlled by the organisation that runs them. Consortium blockchains are governed by the group of organisations that operate them.

How long does a blockchain transaction take?

It depends on the network and how busy it is. A Bitcoin transaction typically takes 10 minutes to get its first confirmation, though full settlement is usually considered to require six confirmations, which takes around an hour. Ethereum transactions confirm in seconds to minutes under normal conditions. Proof-of-stake networks tend to confirm faster than proof-of-work networks.

Is blockchain only used for Bitcoin?

No. Bitcoin was the first blockchain application, but the technology now underpins thousands of cryptocurrency networks, enterprise supply chain systems, cross-border payment networks, decentralised finance protocols, and digital identity verification systems. Blockchain is a general-purpose technology for maintaining shared, tamper-resistant records. Its use in Bitcoin is the best-known application but far from the only one.

What is a smart contract on a blockchain?

A smart contract is a program stored on a blockchain that executes automatically when predefined conditions are met. It is written in code and, once deployed, runs exactly as written with no possibility of human interference. A common example is a payment that releases automatically when a delivery is confirmed. Smart contracts are the foundation of decentralised finance and most non-fungible token systems. Ethereum is the most widely used platform for deploying them.